I wrote a few weeks ago about Toys R’ Us’ decision to put its north American businesses into Chapter 11 liquidation. It had made this decision to escape the weight of debt put onto its balance sheet by the private equite company KKR. Now it turns out that much of America’s retail sector is suffering fom the same problem, according to a detailed analysis by Bloomberg.

Around 3,000 stores will open this year, but more than 6,000 will close—and this at a time of high consumer confidence, low unemployment, and economic growth in the US. These factors are normally good for retail, but as Bloomberg notes, “more chains are filing for bankruptcy and rated distressed than during the financial crisis.”

What’s going on? Well, online is probably not the main culprit, although it doesn’t help. Most of the drivers of change are locked up in the financial system.

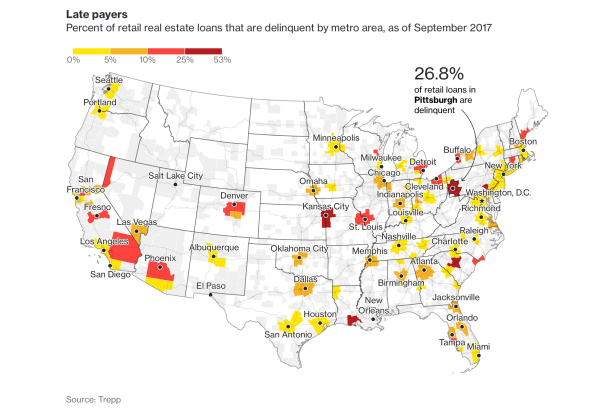

Figure 1: retail retail estate loans going bad

Source: via Bloomberg

Debt levels

The main cause is that the balance sheets of many of the retail chains are, says Bloomberg, “overloaded with root cause is that many of these long-standing chains are overloaded with debt—often from leveraged buyouts led by private equity firms.” As with Toys ‘R’ Us, there are billions of dollars sitting on balance sheets that can’t take that load.

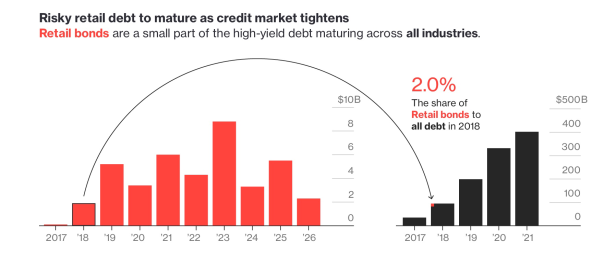

A lot of this debt falls due over the next five years. To give a sense of the scale of this, “$100 million of high-yield retail borrowings were set to mature this year, but that will increase to $1.9 billion in 2018.” And then it ratchets up again, to close to $5 billion a year between 2019 to 2025.

It’s not just the retail sector; for the whole economy high-yield debt is on the increase.

Figure 2: The coming debt bubble (retail, left, all US debt, right)

Source: via Bloomberg

Capital markets

One of the other reasons that retailers have so far avoided the crisis is because interest rates have been so low as a result of the long wave of quantitative easing since the financial crisis. The Federal Reserve is now starting to push rates up, and that means that debt becomes more expensive. In addition, markets are no more sceptical about retail, so lenders will charge them higher interest rates. This has affected even blue-chip retailers like Nordstrom. The article notes that the founding family abandoned attempts to take the department store back into private ownership “because lenders were asking for 13 percent interest”.

The long history

The US had too many stores even in the 1990s, even before e-commerce took off. That is a legacy of over-building retail space when the suburbs were booming. The result was big-box drive-up retailers in every category. Now this demand is unwinding itself. One of the features of retail economics is that as sales slow, and you start approaching the breakeven point at which profits slide into losses, the relatively high fixed costs mean that a blip can turn quickly into a disaster, especially when stuttering performance is squeezing margins. The debt mountain on the balance sheets means that breakeven point is that much higher.

Perfect storm

The result is, in systems terms, a negative feedback loop which has quite a long way to spiral. “That boom,” in Bloomberg’s words, “is finally going bust.” The rate of retail closures this year is running at twice the rate for 2016, and is close to the peak closure year of 2008, in the year of the financial crisis.

The consequences get felt largely by the working poor, for retail is both “the largest employer of Americans at the low end of the income scale” and also a path to the middle class. Supervisors earn twice as much as cashiers, and are often promoted from their ranks. Although there are some compensating job gains in distribution centres, these are much less evenly spread geographically, than retail stores and tend to employ more men than women, so there’s a gender effect here as well. It’s not easy to see other routes to social mobility emerging for less educated workers.

It is clear that American retail is in long-term decline. But one of the lessons of decline is that societies can manage slow decline a lot better than fast decline.

Debt as control

So, reflecting on the Bloomberg article, can we blame private equity companies for behaving like private equity companies? Well, as their defenders would say, they have done nothing illegal here. It is in the nature of finance capital to exploit loopholes, or even to create them, to the advantage of investors and with no regard as to where or on whom the external costs fall. But there is, of course, a deeper point.

It would be easy to construct some balance of “fault” here, about the negligence of political systems that were happy to deregulate finance without creating compensating institutions to protect the rest of us. But, as every systems thinker knows, every system is perfectly designed to produce the outcomes it produces. On one reading, debt is not an unfortunate outcome—I’m drawing here on the work of the Italian sociologist Maurizio Lazzarato— but is an instrument of control, by the finance sector over the rest of society. In Russ Albery’s useful summaryl

The debtor is held to a tight moral standard of repayment of debts, and is morally condemned by all of society, including their peers, for a failure to repay. But there is little or no corresponding moral pressure on the creditor… To be a creditor is to have an agreed-upon, one-sided right to dictate to the debtor the terms on which they must conduct a portion of their life, and the larger the debt, the larger the portion.

Thanks to J Walker Smith for the tip about the article.