A shorter version of this has appeared on my Just Two Things newsletter.

The news last week that Amazon CEO Jeff Bezos planned to step away from the role —albeit to the new post of Executive Chairman—after announcing fourth quarter sales of $125 billion, prompted a long article by the tech blogger Ben Thompson that sat somewhere between panegyric and eulogy, with occasional flashes of hagiography:

He is arguably the greatest CEO in tech history, in large part because he created three massive businesses, all of which generate enormous consumer surplus and enjoy impregnable moats: Amazon.com, AWS, and the Amazon platform… These three businesses are the result of Bezos’ rare combination of strategic thinking, boldness, and drive.

Actual customers

Although the FAANG stocks tend to get lumped together, Amazon, Apple and Netflix are different from the FG: they have actual customers, rather than packaging up their users and selling them on. This was a problem for Amazon (compared to say, Google, which started around the same time):

Amazon had to actually pay for the products it sold! To effectively pursue a tech economics strategy, i.e. bet everything on volume in an attempt to gain leverage on huge fixed costs, was exceptionally risky in an arena with inescapable marginal costs.

One of Bezos’ strengths is that he is curious. Early on he noticed Jim Collins’ concept of the ‘flywheel,’ and got him to spend a few days working with his fledgling executive team. I like the idea of the flywheel—a virtuous circle in which each element of the strategy strengthens the strategy. I’ve sometimes used it with clients to summarise the implications from futures projects. Thompson murders the Amazon flywheel in his article. Jim Collins’ version (which I’ve redrawn) looks like this:

Source: Jim Collins

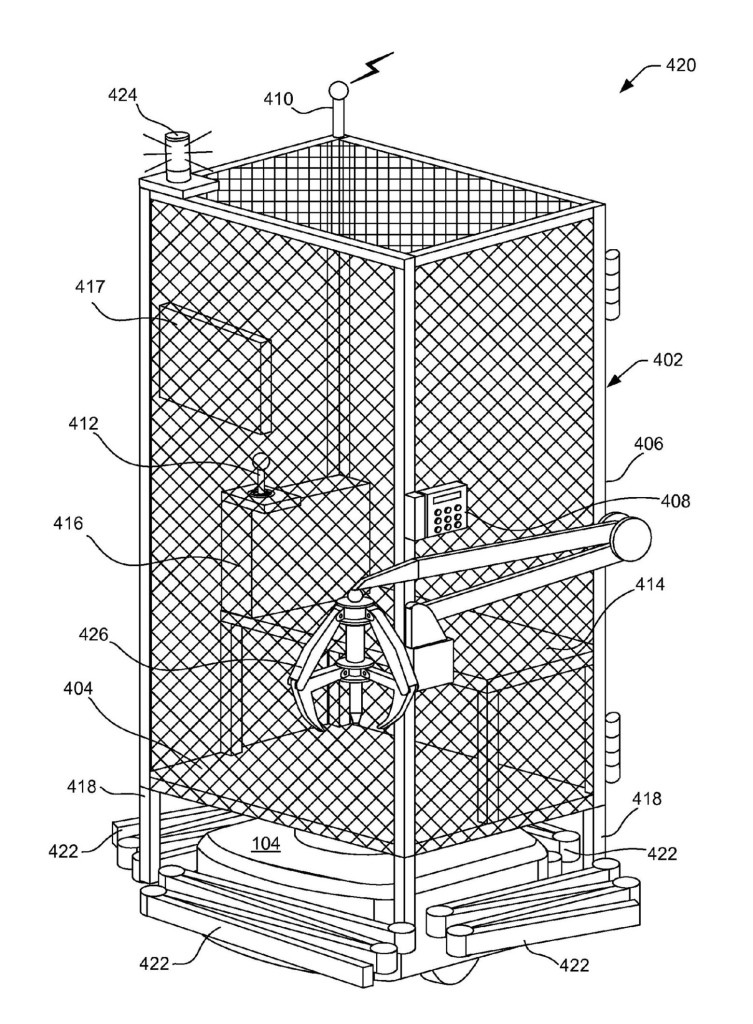

The Cage

Obviously this speaks both to Amazon’s obsessive consumer focus, but also to some of the conflicts of interest that sits in the business model. And, of course, the most lucrative part of Amazon, the software platform AWS, isn’t really part of this circle—it was created to fix a problem, although not everyone would have had the insight to open it up to customers, which built scale and reduced costs. And costs are still, I think, potentially an Achilles Heel for the business.

In an unmissable article on Bezos in the Guardian, the writer Mark O’Connell spent more time than was good for him delving into the Bezos story. For him the Amazon patent for ‘The Cage’, referenced in an art and research project that explored the extractive processes that sit behind the Amazon Echo, goes to the heart of Amazon. Yes: it was never implemented, but this patent was apparently going to put workers inside this, apparently for safer stock-picking purposes.

In its ghostly absence, this structure exemplifies the deal with the devil that you, the customer, enter into every time you click the “Buy Now” button. The true source of your magical power, its true cost, is the life of a worker labouring under deepening conditions of exploitation and control. Stockpickers at Amazon’s warehouses are surveilled and controlled to an extraordinary degree.

Human limitations

For O’Connell, the thinking that sat behind the patent goes to the heart of Amazon’s business:

The cage suggests a way of thinking about what distinguishes Amazon as a business, and Bezos as an innovator: the use of technology to push harder and farther than any previous company toward removing, at both ends of the supply chain, the human limitations to capital’s efficiency.

Sometimes when CEOs step away, it is just because they want to spend more time with their money. But sometimes it is because they know that the business is never going to hit the same heights again. (Think Bill Gates at Microsoft or Terry Leahy at Tesco).

Predatory

So it is worth asking: what grit is out there that might clog up Amazon’s wheel?

Well, there are a few things.

Ben Evans mentions a couple of them in his long recent presentation “The Great Unbundling”. The first is that big customers abandon the Amazon Market and do their own thing, as Nike has done. The second is that we’re moving into an era of tech industry regulation, in both Europe and the US.

Amazon has a clear history of predatory pricing, as Jacobin noted last week, in its account of how the company forced Diapers.Com to sell to it. The current EU case against Amazon is in a similar space: that Amazon uses the information it gains from Amazon Market to compete against sellers as a retailer. The House of Representatives’ tech report comes to a similar conclusion. In most markets where this happens, this is a clear conflict of interest—it’s not inconceivable that the EU will force the company to choose between them if it wants to do business legally in the EU.

Corporate culture

Then there is the issue of the corporate culture, which is toxic even for those in the head office, but far worse for those in the warehouses.

The company did raise minimum wages in the US and the UK, likely for self-interested reasons to do with tight labour markets and high turnover rates, but 4,000 Amazon workers across nine states in the US are on food stamps. The company is well-known for its anti-union activities, and is evasive about these when caught out. The company’s done everything it can to prevent or delay an impending vote on unionisation in an Alabama warehouse. But then again: companies that care about employment standards don’t feel the need to retain the notorious agency Pinkerton’s to counter workers who are trying to organise. That kind of thing comes from the top.

Amazon’s workplace injury rates run at twice the US national average. Vice reports that “injury rates are highest during Amazon’s peak season in the lead-up to Christmas, when standard shifts extend for 10 to 12 hours a day.” The National Law Employment Project noted in 2020 that “Amazon has topped the National Center for Occupational Safety and Health’s (NCOSH) “Dirty Dozen” list of employers who put workers and communities at risk for two years straight”.

And in interviews, former and current Amazon delivery drivers “almost universally reported speeding or violating other traffic laws to keep up with their daily delivery quotas”.

Taxes

Amazon seems to push down local wages when it opens new warehouses or distribution centres in your area, which may become more significant as local politicos become more sophisticated in thinking how best to build local economies.

And of course, it’s not very good at paying taxes. This may become more important for national Treasury departments as they deal with lockdown debts. In fact, the Fair Tax Mark found they were the worst tax avoider (pdf) even among the Tech Giant’s club. (Yes, I’m sure that what they do is “perfectly legal.” But that’s not the point).

One of the quotes that Bezos is famous for is the things that aren’t going to change. He’s said versions of this on multiple occasions:

Bezos said people often ask him to predict what will change over the next decade, but asking what won’t change over 10 years can offer potentially more valuable insight… For Amazon, the obvious answer is that customers will always want low prices, fast shipping and a large selection.

When the management thinker Peter Drucker said that the first task of business is to create a customer, he didn’t mean that it was the only task. Drucker also observed that “the theory of the business” is “a hypothesis about things that are in constant flux—society, markets, customers, technology.”

Logistics

Amazon’s theory of the business—seen in both the flywheel and in Bezos’ assertion about what won’t change—is dependent on a huge logistics infrastructure. One racing certainty over the next decade is that the carbon cost of this is going to increase, possibly quite quickly. Transport always has a higher emissions cost when it’s faster and more complex, and especially when planes are involved. It’s possible Amazon will end up with trade-offs between speed and price, or two-tier delivery systems.

In other words, there are externalities everywhere. When we look back at Jeff Bezos’ career, we’ll see someone who spotted the internet early, and rode it brilliantly. But we’ll also see an old-fashioned 20th century American tycoon, someone who did whatever he could to make sure that the costs his businesses generated ended up being paid by other people. There are good reasons to think this is coming to an end. It might be just the moment to kick yourself upstairs.