Like everyone else I have been trying to work out what to make of the GameStop bubble as it blew up last week. These are some notes from my reading over the week. I’ve been helped here by my son Peter, who sometimes hangs out in the reddit subgroup that has caused some of the trouble, and who wrote a nice explainer last week on his Substack.

My best take is this: that it represents one of those conjunctions of weak signals that you sometimes see when you use Wendy Schultz’s Manoa method, that combine to create unanticipated outcomes that are explicable in hindsight but hard to see, at least in detail, in advance.

Locusts

The first is: the hatred of forms of extractive “locust” business (pdf) represented by hedge funds is real. It hasn’t declined over time. From Peter’s substack:

[O]ne interesting facet of this whole avalanche of trading is the hostility shown towards anyone in ‘traditional’ finance world. This isn’t just about GME, there’s a real sense of injustice. One user comments:

“These are the same kind of guys that got bailed out while people lost all their pensions and life savings in ’08. I don’t even care about the money anymore, I just want to know we actually made a stand and tried to make a difference if this doesn’t work out.”

But how much better to be able able to make some free money at the same time.

Loosely coupled

Second, it’s an expression in the finance sector of the same kinds of directed but loosely coupled engagement that the internet enables and which is more familiar in politics. James Surowiecki compared it to some of the grass-roots political campaigns that supported Trump in 2016:

What [the alt-right] did, in effect, was exploit the opportunities created by social media to disrupt the normal workings of the political system, at least in part for the lolz. The traders on r/Wallstreetbets — which describes itself, tellingly, as “Like 4chan found a Bloomberg Terminal” — are trying to do the same thing to Wall Street.

How are they doing it? By embracing companies that Wall Street, for good reason, hates: beaten-down firms in legacy businesses with weak economic fundamentals.

Third, and most obviously, it’s a function of the democratisation of access that happens over time with technologies (and not just digital ones). Technologies start in the business and professional world, and move to the consumer world. It’s just a function of the cost curve.

Casino capitalism

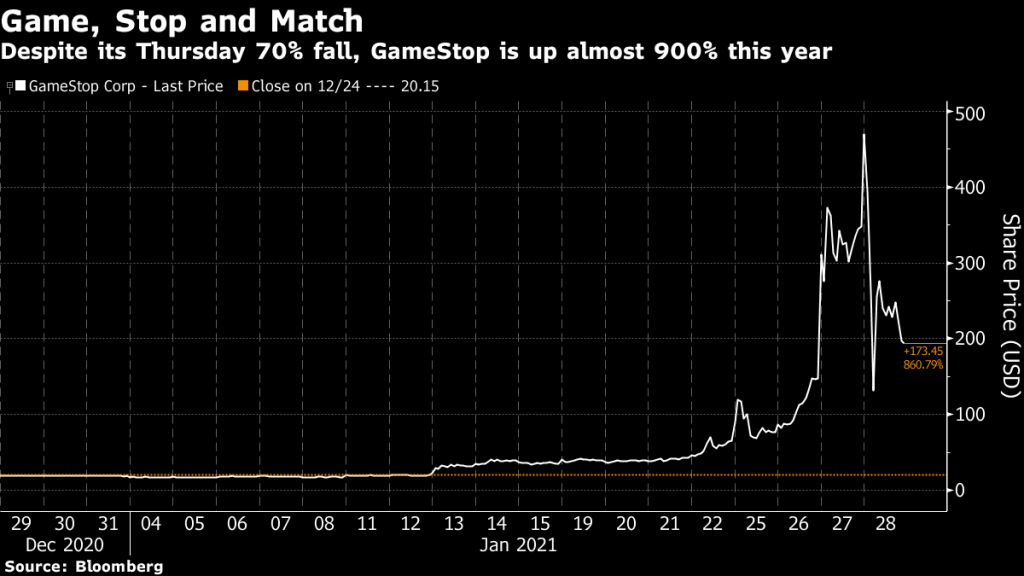

One of the outcomes, though, is that it has reminded people of Keynes’ famous observation that stock markets are casinos. At a point when the pandemic has pulled the curtain away from the wizard, spelling this out so starkly has political consequences. Clearly markets where a middle of the road video game retailer is worth $25 billion are not functioning properly, as John Authers noted at Bloomberg.

But, as Matt Taibbi argued in a hilarious piece in his newsletter, the stock markets haven’t really been functioning properly since the 2008 bailouts and quantitative easing put lots of free money into the financial system, and pandemic bailouts have just made this worse:

The constant in the bailout years has been a battery of artificial stimulants sent through the financial sector, from the TARP to years of zero-interest-rate policies (ZIRP) to outright interventions like the multiple trillion-dollar rounds of Quantitative Easing. All that froth allowed finance companies to suck out hundreds of billions in fees, encouraged lunatic risk-taking in every direction and rampages of private equity takeovers, and kept a vast stable of functionally dead companies alive on cheap credit.

Funhouse economy

So the sight of the captains of Wall Street, former regulators, and politicians such as Nancy Pelosi (who ought to know better) queuing up to express their concern is just a little bit rich. Especially since the finance sector has had a wonderful year at everyone else’s expense off the back of the 2020 bailouts. Taibbi again:

While policymakers may have stabilized the economy with the bailouts, they may also “inadvertently be directing the flow of capital to unproductive firms,” as Bloomberg euphemistically put it back in November. In other words, it was all well and good for investment banks and executives of phoney-baloney companies to gorge themselves on funhouse profits on a funhouse economy, but when amateurs decided to funnel just a bit of this clown show into their own pockets, finance pros wailed like the grave of Adam Smith had been danced upon.

Nor should we think of stock markets as being a signal to meaningful economic information. As Peter Radford says, at Real World Economics Review:

“Then, of course, there’s the argument that stock prices are indicative of a notion of future economic activity… More likely, the stock market reflects the collective wisdom of the wealthy elite as to where it thinks its future rents can be extracted.”

But as John Authers observes: doing anything about all of this that benefits Wall Street in general, and hedge funds in particular, at the expense of redditors or other individual investors, is political poison. And rightly so.

A version of this post also appears on my Just Two Things newsletter.