“Yes, as through this world I’ve wandered

“Yes, as through this world I’ve wandered

I’ve seen lots of funny men;

Some will rob you with a six-gun,

And some with a fountain pen

(‘Pretty Boy Floyd‘, by Woody Guthrie)

It’s hard to watch the whole bank bonus row unfold without thinking that it seems to be taking place in a social and economic void. To pump some air in, I thought I’d try the ‘Five Whys‘ approach to unpack it a bit.

Why can banks afford to pay huge bonuses? Because they make huge profits.

Why do banks make huge profits? Because the legal, regulatory, economic and political environment has increasingly been stacked in their favour over the last thirty years.

Why has the external environment been stacked in their favour? Well, I had a go at answering that question here, recently, but it’s worth spending some time on the first couple of questions. The answer, at least on one account, is that banks have systematically offloaded risk onto the state. Which, given that they’ve now been bailed out to the tune of billions without having to pay back their previous (or future) profits seems like a fantastically successful business operation; nice work if you can get it.

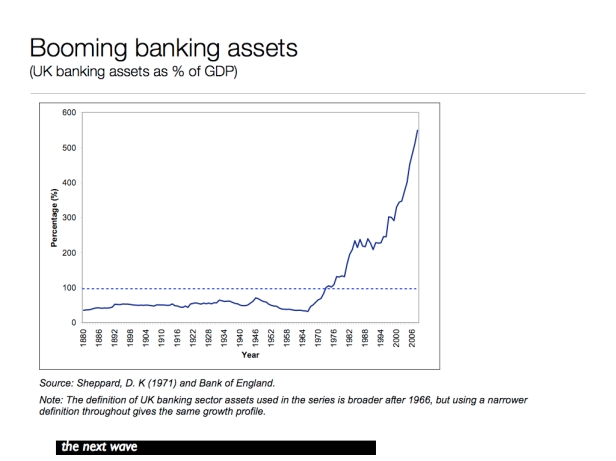

You don’t have to take my word for this. Turn instead to a recent paper (opens in pdf) by an Executive Director of the Bank of England, Andrew Haldane, written with Piergiorgio Alessandri. He argued at Federal Reserve Bank of Chicago’s recent conference, on “The International Financial Crisis: Have the Rules of Finance Changed?”, that the banking system had become the main source of ‘sovereign risk’ to the state. There are some startling data – first, the speed at which the sheer scale of banking assets have exploded over the past 30 years, and are now five times as great as British GDP. It isn’t a surprise, of course. But it confirms what you already know – that the banking sector is far too large compared to the non-financial economy, which it is supposed to service.

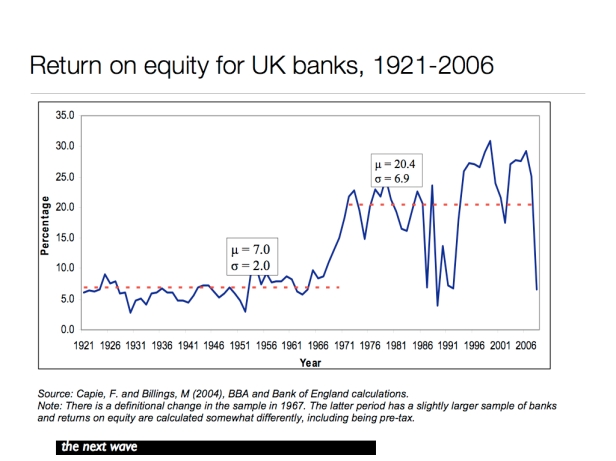

Even more striking is the rise in profitability of the banks, from a long-term rate of around 10% for much of the 20th century, to 30% for most of the last forty years. And with the increase, much greater volatility.

At this point it’s probably worth pausing to observe that in competitive markets the rule of thumb is that the general rate of profit will be around 10%. If it’s more, new competitors think it worth entering the market; less, and poorly performing companies go out of business. So a sector which is making 30% has gained some kind of exceptional advantage.

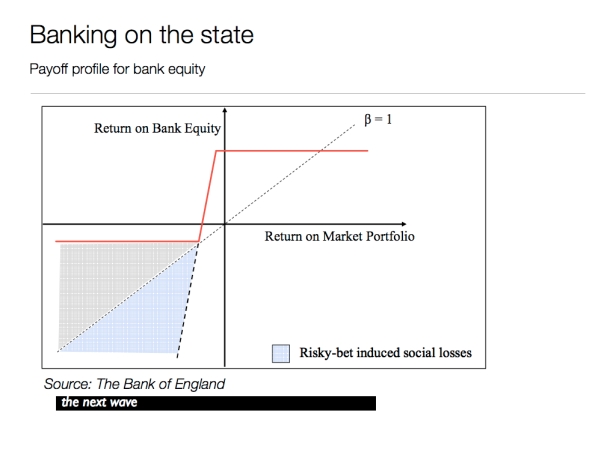

Haldane suggests that in fact the banks have gained several advantages. They’ve shrunk their capital ratios (the amount of money they hold in reserve against their lending); they’ve transferred funds to their (higher risk) trading portfolios; they’ve invested in higher reward, but higher risk, assets. And they’ve done this because they’ve made a big bet that if it all goes horribly wrong, the state will bail them out. Without getting too far into the technicalities of the diagram, the 45 degree line is ‘normal’ banking, while the red line is banks ‘gaming’ the system by excessive risk taking. Effectively, the diagram shows how banks have offloaded their risk to the state.

Betting against the state

The important point here is that this isn’t a single game – it’s a system in which the banks test the state over time. If Keynes compared the working of the stock market to a casino, Haldane suggests that the banks’ strategy is like the St Petersburg paradox – a gambling strategy in which you double your stake every time you lose.

The St Petersburg lottery has many similarities with the game played between the state and the banks over the past century or so. The banks have repeatedly doubled-up. And the state has underwritten any losing streak.

This works, for the banks, because they know the state won’t let them go bust. But it’s certainly not good for the rest of us. As Haldane says,

Socialised losses are doubly bad for society. Taxes may not only be higher on average. They may also need to rise when they are likely to be most painful to taxpayers, namely in the aftermath of crisis. So taxes profiles will be spiky rather than smooth and will spike when the chips are down. This is the opposite to what tax theory would tells us was optimal.

There are things which the state can do here, even without executing bankers (as states gave done in the past) or removing limited liability from bank shareholders (which would change their risk appetite quickly). They can – quite quickly – require banks to increase the size of their capital reserves, and to pay more for the service supplied by the state of insuring banks against collapse (one of the emerging arguments for the Tobin tax). Haldane also suggests that it’s time to address the excessive concentration in the banking sector: “In 1998, the five largest global banks had around 8% of global banking assets. By 2008, this fraction had doubled to around 16%”. And he makes a striking comparison with hedge funds, where there is far less concentration (and declining), and far greater entry and exit in and out of the sector; coincidentally, or not, operating without state guarantees and without limited liability.

Paying for money

These things might reduce the excessive profitability of the banking sector, although some critics think we need to go further to return it to an apprporiate scale and to normal levels of profit. James Robertson has long argued that because most money in circulation is created by the banks when they create credit, effectively they are getting their raw materials for free – unlike other sectors. And the circulation of money is a social function, so there’s no reason why they shouldn’t buy their raw materials from the rest of us. Technically this wouldn’t be complex; one would return the power to create new money back to the Bank of England, and remove it from the commercial banks. The banks would hate it of course, but there would be a substantial social bonus – elsewhere, Robertson has estimated that the public gain in the UK from selling money to the banks rather than giving it to them would be of the order of £45 billion, a year. To put that sum in context, the government’s record breaking deficit this year, to bail out the banks, is £178 billion, and the National Insurance increase announced today will raise £3 billion in a full year. Or it could fund a citizen’s income of about £1,000 a year for every adult in the country, with all the benefits which follow for social equity.

This is a fantastic article which really helped me pass some tiem this sunday evening in the Uk.

My personal opinion about the banks is that they are the ones that caused the credit crunch and the recession in the uk but thats another kettle of fish.

Cheers James