Cliches become cliches because they catch a truth. And one of the cliches of COVID-19 is that pandemics expose your weaknesses. And so it has. The pandemic has made visible, quickly, weaknesses in our economies that critics have been warning about for years, but which have been accumulating too slowly for governments to care about their impacts.

The economics crisis is about to hit us. We are in that moment before the tsunami rushes in, when the water retreats and exposes the sea floor.

Economic weaknesses

These weaknesses, certainly in the British economy, can be summarised quickly: low wages and and an over-casualised workforce; low productivity; low investment; a property sector that has got used to over-generous rents; an over-reliance on services and a lack of manufacturing capacity; too much dependence on the extended logistics of a global supply chain. National economies have become addicted to government stimulus, as Adam Tooze reminds us. I may have missed some. But in short, the crisis was coming anyway, but would have taken several years to arrive.

And the fact of that the crisis is a sudden crisis is a good thing. Governments and politicians are terrible at thinking about slow-moving long-term problems, but know that they need to respond to emergencies.

The scale of shock

It’s hard to gauge the size of the economic shock, but it’s going to be big. The Bank of England sees the biggest collapse in a single year since 1709, although to my eyes it is also recklessly optimistic about the rate of recovery. It’s possible to imagine that this is a piece of ‘performative forecasting,’ designed both to appear realistic and not to spook the markets.

But people who know more about pandemics expect that the economic shock will continue, in some form, for between 24 and 36 months, which points more to a ‘U-shaped’ economic shock, or a ‘W’, rather than the Bank of England’s deep ‘V’.

Range of estimates

The range of estimates in terms of hit to GDP is wide. The best case estimate is probably of the order of 10%, or about the scale of the shock in Western economies in the wake of the Global Financial Crisis. But it could also be as high as 30%, which puts it deep into Great Depression territory, and beyond. Evidence for a larger slump includes the large and rapid contraction in world trade. Of course, we know much more about macro-economics than we did then, and have better tools. But this does not remove the risk of wilful blindness, or policy error.

For my mental models on this, I have been working with three scenarios. Professional caveat: these are not the result of a detailed scenarios development process. More, they are based on analysing the underlying dynamics of a world living with this scale of economic shock.

1. Wilful blindness

The first of these scenarios might be called Wilful Blindness. This is, effectively, a re-run of the post-financial crisis approach. Governments do ‘whatever it takes’ in the moment of the crisis, but then decide they can’t live with the public debt levels that have resulted. And so we see a rerun of austerity, and so on.

This would certainly be a policy mistake, but it also a less feasible option than it was in the UK in 2010. One reason is that private and corporate debt is also high, so public sector retrenchment would likely lead to a cascade of private sector failures, worsening the situation the government finds itself in.

Magic money trees

Another is that the Reinhart and Rogoff analysis, which gave technocratic cover to ideologically austerian governments, turned out to be wrong. (Their work suggested that when government debt climbed about 90% of GDP, growth slowed dramatically. Shame about the rookie spreadsheet errors.)

And a decade of quantitative easing, and the current pandemic spending, has also put a big pin in the ‘no magic money tree’ argument. It’s also shown that countries that control their own currencies can magic up surprising amounts of money without experiencing inflation, contrary to the earlier expectations of mainstream economists.

‘We didn’t deserve this’

The final reason is that people who are hungry and destitute are less forgiving of their governments than people who are not. One of the things I noticed in some news coverage was an interview with a now unemployed middle class man who told the interviewer:

“We didn’t deserve this. It’s not out fault.”

Critics of capitalism would argue that this is almost always true, but that one of the tricks that capitalism plays is to get people to internalise personal blame for its systemic vagaries. This is harder when a lot of people have a shared experience of being on the wrong end of those vagaries.

Some countries will still try this scenario, if only because it takes a long time for failed policy paradigms to die off. But it’s not stable; it will fissure.

2. New corporatism

The second scenario is, broadly, ‘a new corporatism’. This might be shorthanded as Orbanism with Chinese surveillance characteristics. So we have populist leaderships playing the nationalist card deck, doing a lot of othering, and also—potentially under cover of the public health emergency—imposing a lot of surveillance. This might start as semi-voluntary but probably wouldn’t stay that way.

This is one of the reasons why the current discussion about contact-tracing apps is so polarised. It’s not just about contact tracing.

Corporate workfare

This scenario still has to deal with the problem of large numbers of hungry and destitute people. I’d expect to see large amounts of what I’d call “corporate workfarism”, under which people are paid minimum living wage for apparently socially useful work (maintaining parks, sweeping streets, working as school assistants), no doubt managed by outsourcers such as Capita on behalf of the government.

There would also be random eye-candy type investment in infrastructure projects that pandered to headlines, but it would be unlikely to be coherent, or to produce a decent rate of return. This could take the form of some glossy technology projects that do more for the surveillance than for the liveability, but aren’t sold or positioned that way. Maybe there’s quite a lot of pork-barrel cronyism on display as well.

Creating dissension

This scenario wouldn’t generate any sense of long-term energy, or much economic growth. It’s a low wage, low productivity scenario. In the long run, this tends to be its undoing. It also depends on creating dissension between different groups. But populists have shown that they are effective at doing this. It could sustain for a while. (Think of the duration of pre-digital corporatist regimes like that of Franco or Salazar.)

3. Purposeful investment

The third scenario is about “purposeful investment.” The government sets out to rebuild the economy by investing in the infrastructure needed to move to an economy based on renewables, and probably invests in other bits of the crumbling infrastructure (schools, public housing) at the same time.

Unlike in 2008-2010, this scenario now has the investment numbers on its side. The energy journalist and analyst Gregor McDonald noted in Buzzfeed :

[T]he real story is that we’ve already seen [in the US] huge payoffs on the relatively modest investments made on clean energy… Better still, as costs continue to crash, job creation has exploded. Renewable energy industries in the US employed 4 million people by 2016, according to the Environmental Defense Fund — far more than the coal industry.

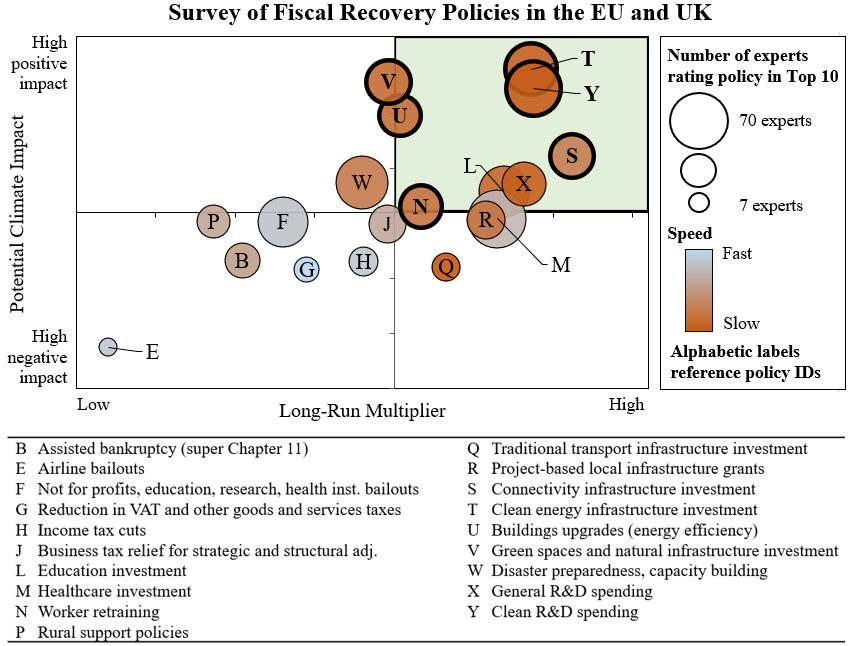

De-carbonising

A survey of 230 economists by Oxford’s Smith School found a consensus that government spending on decarbonising spending had the most effect in terms both of short-run multiplier effects and medium-to-long run impact.

Sea of capital

There’s more here as well. One of the legacies of quantitative easing is that we are awash in a sea of capital that is unable to find a return. This is at a time where we need long-term returns to be better if we are to fund the economic and social commitments that our ageing population will generate.

The Marxist geographer David Harvey observed in his book Rebel Cities that public infrastructure investment is a classic response to the problem of excess capital, when you look back through history. He references Haussmann’s rebuilding of Paris and Robert Moses’ role in post-war New York.

Narrow interests

Of course, there are problems with this scenario as well. One is that, certainly in the UK, the party of government has become completely detached from the interests of capital, at least beyond the narrow interests of speculative investment.

The second is that an economy that has de-prioritised technical and productive skills for so long might have problems finding the skills and labour to implement this approach.

Underlying economics

The third is that the outlines of this programme look like the proposal also known as “the Green New Deal,” which is associated with the left in both the US and the UK. This means that it is misread as a social and environmental programme in which the economic outcomes are secondary, not one which aligns all three outcomes.

As Wired reported recently:

Since 2010, the cost of generating solar electric power has dropped by 80 percent, and gigantic photovoltaic plants, some spanning thousands of acres, are transforming the economics of green energy… “We’re reaching a phase where it’s cheaper to build a new solar power plant than it is to operate an existing coal one,” says energy investor Ramez Naam.

But people still pigeon-hole it as “green costs money,” especially if they haven’t noticed how fast the underlying economics have shifted. On the face if it, it’s a mystery why financial interests aren’t pushing for this scenario, which is clearly in their interests. But it’s not that much of a mystery: groups of people with conservative worldviews who herd together take a long time to change those views, even when the underlying facts change.

Signs of change

All of that said, there are some signs that some of this is beginning to change.

One of the clear lessons from the COVID-19 crisis is that there wasn’t a trade off between health and economics. Countries that prioritised health and responded rapidly to the virus, such as South Korea, China, even Greece, were able to get their countries started again quickly.

Countries such as the UK and the US, that constructed a dichotomy between looking after health and looking after the economy, have had worse health outcomes and will likely have worse economic outcomes.

Social learning

There’s also evidence of social learning: the countries that went through the SARS crisis have been the best models to copy this time around–at least for anyone not wedded to the myth of national exceptionalism.

The public health crisis also constructs a different relationship between the economy and health, although you might miss this if you spend too much time listening to economists. Effective production, and effective markets, require a healthy workforce. But the social reproduction of health is simply taken for granted in economic models. (And in most labour market models as well).

Mike Davis put this starkly in the most recent issue of New Left Review:

[C]apitalist globalization now appears to be biologically unsustainable in the absence of a truly international public-health infrastructure.”

The limits of economics

And, of course, the limits of the market have become much clearer since the pandemic struck, along with the social and public conditions (and laws and rules) that make them work they do. Obviously, the standout example of this was the Financial Times’ (paywalled) interview with President Macron:

It puts the human back in the middle. It’s clear that economy is no longer the priority. And when it’s a matter of humanity, women and men but also the ecosystems in which they live, and so CO2, global warming, biodiversity, there is something more important than the economic order.

Similarly, Diane Coyle has suggested (I paraphrase) that the crisis has reattached the idea of ‘moral’ to ‘economy’:

As the pandemic has demonstrated, however, it is… everyday economic activities, that reveal the collective, connected character of modern life beneath the individualist façade of rights and contracts.

This has been a theme ever since the pandemic arrived. It is deeply at odds with the individualist and exceptionalist politics of populism that has been so strident over the last decade. Public health crises, for all their unequal effects, remind us that we are more alike than different. We’re going to be reminded of this a lot over the next 24 to 36 months.