Planning for retirement might seem like a distant goal, but the earlier you start, the more secure your financial future will be. Whether you’re just beginning your career or nearing retirement age, it’s never too late to take control of your savings and ensure a comfortable lifestyle in your golden years.

In this guide, we’ll walk you through everything you need to know about saving for retirement in 2025, including actionable steps, tools, and strategies to help you achieve your goals.

Why Saving for Retirement Is Essential

Retirement planning is not just about stopping work—it’s about maintaining your quality of life without financial stress. Here’s why it’s crucial:

- Longer Lifespans : People are living longer, which means you’ll need more money to cover expenses during retirement.

- Uncertain Social Security : Relying solely on Social Security may not be enough to sustain your desired lifestyle.

- Rising Healthcare Costs : Medical expenses tend to increase as you age, making it essential to have a financial cushion.

- Peace of Mind : Knowing you have a solid retirement plan reduces stress and allows you to focus on enjoying life.

How Much Do You Need to Save for Retirement?

The amount you need to save depends on several factors, including your desired lifestyle, expected expenses, and retirement age. Here’s how to estimate your target:

Use the 4% Rule

This rule suggests withdrawing 4% of your retirement savings annually to make them last. For example, if you want $40,000 per year, you’ll need $1 million saved.

Consider Your Expenses

Estimate your monthly expenses in retirement (housing, healthcare, travel, etc.) and multiply by the number of years you expect to live in retirement.

Factor in Inflation

Account for rising costs over time. A dollar today won’t have the same purchasing power in 20 or 30 years.

Set Realistic Goals

Break your savings goal into smaller milestones. For example, aim to save $100,000 by age 40, $300,000 by age 50, and so on.

Step 1: Start Early and Leverage Compound Interest

One of the most powerful tools for retirement savings is compound interest . The earlier you start, the more time your money has to grow.

How It Works :

- Your initial investment earns returns, and those returns generate additional earnings over time.

- Example: If you invest $200/month starting at age 25, you could have over $500,000 by age 65 (assuming a 7% annual return).

Why It Matters :

- Delaying retirement savings by just 5 years can cost you tens of thousands of dollars in lost growth.

Step 2: Choose the Right Retirement Accounts

There are several types of retirement accounts to consider, each with unique benefits. Here are the most common options:

401(k) Plans

- Employer-sponsored plans that often include matching contributions.

- Contributions are tax-deferred, meaning you pay taxes when you withdraw funds in retirement.

IRAs (Individual Retirement Accounts)

- Traditional IRA: Contributions may be tax-deductible, but withdrawals are taxed.

- Roth IRA: Contributions are made with after-tax dollars, but withdrawals are tax-free.

Health Savings Accounts (HSAs)

Triple tax advantages: Contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are tax-free.

Brokerage Accounts

Flexible, non-retirement accounts for investing in stocks, bonds, or ETFs. While they don’t offer tax advantages, they provide liquidity and flexibility.

Step 3: Maximize Employer Contributions

If your employer offers a 401(k) match, take full advantage of it—it’s essentially free money.

Example :

- If your employer matches 50% of your contributions up to 6% of your salary, contributing at least 6% ensures you’re maximizing their contribution.

Pro Tip :

- Even if you can’t contribute the maximum allowed, aim to contribute enough to get the full match.

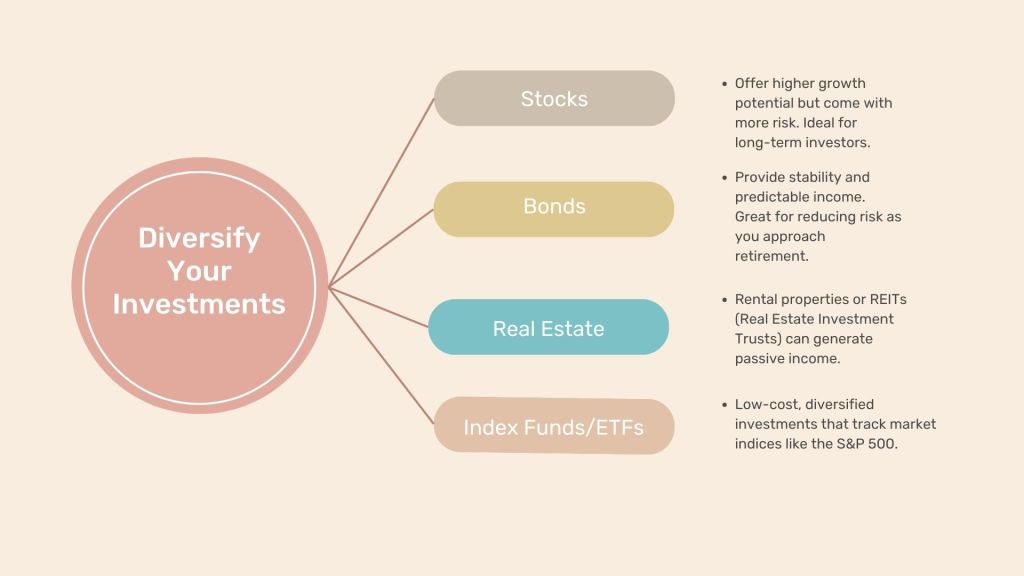

Step 4: Diversify Your Investments

A well-diversified portfolio helps protect your retirement savings from market volatility. Here’s how to diversify:

Stocks

Offer higher growth potential but come with more risk. Ideal for long-term investors.

Bonds

Provide stability and predictable income. Great for reducing risk as you approach retirement.

Real Estate

Rental properties or REITs (Real Estate Investment Trusts) can generate passive income.

Index Funds/ETFs

Low-cost, diversified investments that track market indices like the S&P 500.

Step 5: Adjust Your Plan Over Time

Your retirement plan isn’t set in stone. Regularly review and adjust it to stay on track:

- Rebalance Your Portfolio : Ensure your asset allocation aligns with your risk tolerance and timeline.

- Increase Contributions : As your income grows, contribute more to your retirement accounts.

- Plan for Healthcare : Research Medicare options and consider long-term care insurance.

Secure Your Retirement Today

Saving for retirement doesn’t have to be overwhelming. By starting early, choosing the right accounts, and staying consistent, you can build a secure financial future.

Leave a comment