Your credit score is one of the most important numbers in your financial life. It determines whether you qualify for loans, credit cards, mortgages, and even rental applications. But what exactly is a credit score, and why does it matter so much?

In this guide, we’ll break down everything you need to know about credit scores, including how they’re calculated, why they’re important, and how you can improve yours step by step.

What Is a Credit Score?

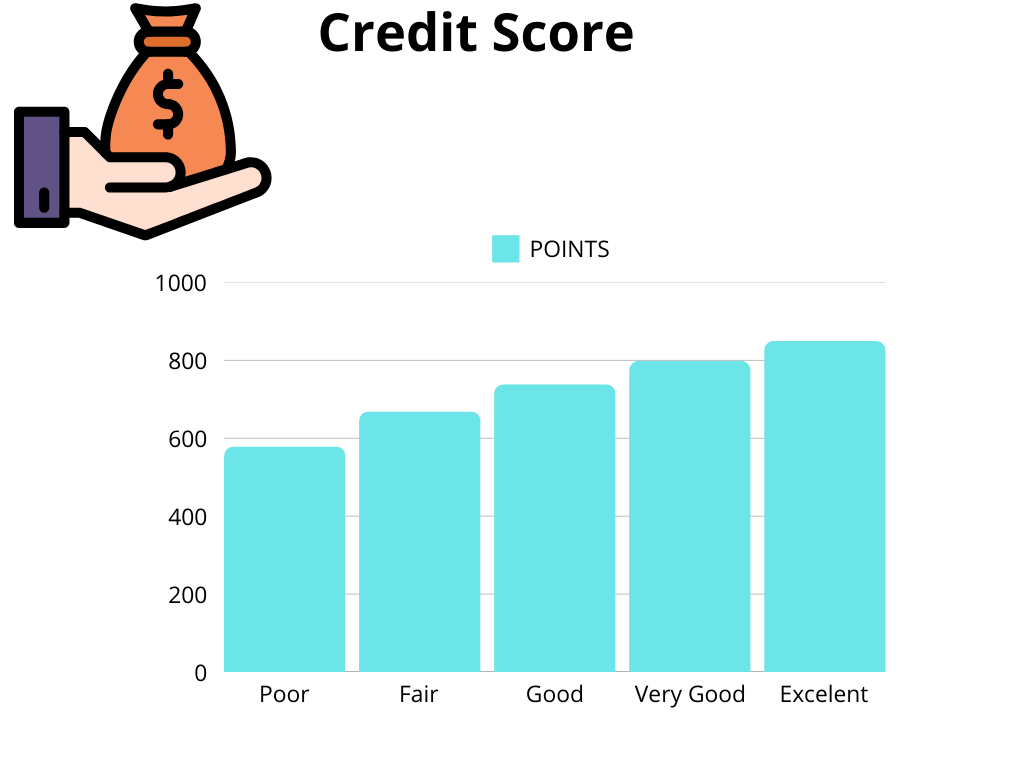

A credit score is a three-digit number that represents your creditworthiness. Lenders use it to assess how likely you are to repay borrowed money on time. In the U.S., the most commonly used credit scoring model is the FICO score , which ranges from 300 to 850.

Here’s what the ranges mean:

- 300–579 : Poor

- 580–669 : Fair

- 670–739 : Good

- 740–799 : Very Good

- 800–850 : Excellent

Why Does Your Credit Score Matter?

Your credit score affects nearly every major financial decision you make. Here’s why it’s so important:

- Loan Approvals : A higher score increases your chances of qualifying for loans with lower interest rates.

- Credit Card Offers : Better scores unlock premium credit cards with rewards, cashback, and travel perks.

- Renting a Home : Landlords often check credit scores to assess reliability.

- Insurance Rates : Some insurers use credit scores to determine premiums.

- Employment Opportunities : Certain employers review credit reports as part of background checks.

In short, a good credit score opens doors, while a poor one can limit your options and cost you more money in the long run.

How Is Your Credit Score Calculated?

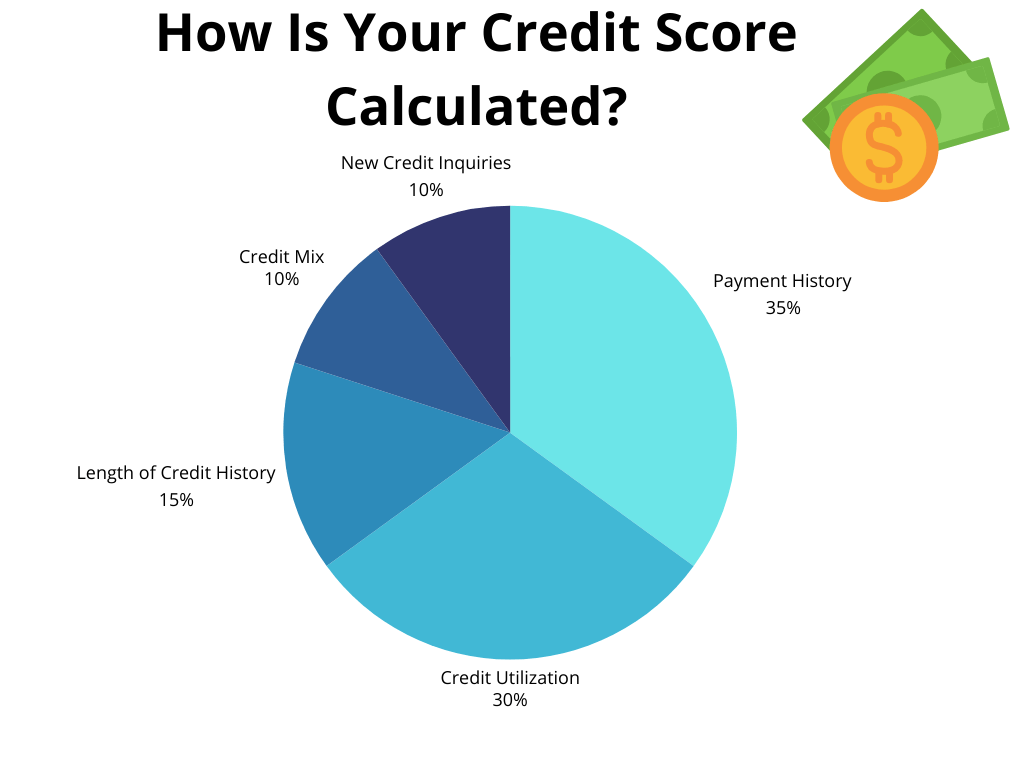

Your credit score is based on five key factors, each weighted differently. Understanding these factors can help you improve your score over time.

Payment History (35%)

This is the most important factor. Lenders want to see that you pay your bills on time. Late payments, collections, and bankruptcies can significantly hurt your score.

Credit Utilization (30%)

This measures how much of your available credit you’re using. Experts recommend keeping your utilization below 30% (ideally under 10%) to maintain a healthy score.

Length of Credit History (15%)

The longer your credit history, the better. This includes the age of your oldest account, the average age of all accounts, and how recently you’ve used credit.

Credit Mix (10%)

Having a mix of credit types—such as credit cards, installment loans, and mortgages—shows lenders you can manage different types of debt responsibly.

New Credit Inquiries (10%)

Each time you apply for credit, a hard inquiry is recorded. Too many inquiries in a short period can lower your score.

How to Check Your Credit Score

Knowing your credit score is the first step toward improving it. Here’s how you can check it for free:

- Credit Reports : You’re entitled to one free credit report per year from each of the three major credit bureaus (Equifax, Experian, TransUnion) at AnnualCreditReport.com .

- Credit Monitoring Tools : Apps like Credit Karma, Mint, or Experian offer free credit monitoring and updates.

- Bank or Credit Card Providers : Many banks and credit card companies now provide free credit scores to their customers.

Actionable Tips to Improve Your Credit Score

Improving your credit score takes time, but small, consistent actions can make a big difference. Here are some practical steps to get started:

Pay Bills on Time

Set up automatic payments or reminders to ensure you never miss a due date.

Reduce Credit Card Balances

Pay down existing balances to lower your credit utilization ratio.

Avoid Opening Too Many Accounts at Once

Limit new credit applications to avoid multiple hard inquiries.

Keep Old Accounts Open

Closing old accounts can shorten your credit history and increase your utilization ratio.

Dispute Errors on Your Credit Report

Check your credit report regularly for errors and dispute any inaccuracies with the credit bureaus.

Common Myths About Credit Scores

here’s a lot of misinformation about credit scores. Let’s debunk some common myths:

- Myth 1: Checking Your Credit Score Hurts It

False. Checking your own score is a soft inquiry and doesn’t affect it. - Myth 2: Closing a Credit Card Improves Your Score

False. Closing a card can actually hurt your score by increasing your credit utilization. - Myth 3: Income Affects Your Credit Score

False. Your income isn’t a factor in your credit score, though it may affect your ability to get approved for credit.

Understanding these truths can help you make smarter financial decisions.

Start Building a Stronger Credit Score Today

Improving your credit score is a journey, not a sprint. By understanding how credit scores work and taking proactive steps, you can unlock better financial opportunities and achieve greater financial freedom.

Ready to take control of your credit? Download our free Credit Score Improvement Checklist to track your progress and stay on track.

Leave a comment