Your credit score is one of the most important numbers in your financial life. It affects your ability to borrow money, rent an apartment, buy a car, or even land a job. In 2025, understanding your credit score is more critical than ever as lenders, landlords, and employers increasingly rely on it to make decisions.

In this comprehensive guide, we’ll walk you through everything you need to know about your credit score in 2025 , including how it’s calculated, why it matters, and actionable steps to improve it. Let’s dive in!

What Is a Credit Score?

A credit score is a three-digit number that represents your creditworthiness. It tells lenders how likely you are to repay borrowed money based on your past financial behavior.

Why It Matters

- Lending Decisions : Banks and credit card companies use your credit score to determine whether to approve your application and what interest rate to offer.

- Renting : Landlords often check credit scores to assess whether you’re a reliable tenant.

- Employment : Some employers review credit reports as part of the hiring process, especially for roles involving financial responsibility.

- Insurance Rates : Insurers may use credit scores to set premiums for auto or home insurance.

Types of Credit Scores

There are several credit scoring models, but the most widely used is the FICO Score (Fair Isaac Corporation). Other models include VantageScore , which is gaining popularity. Both range from 300 to 850 , with higher scores indicating better creditworthiness.

How Is Your Credit Score Calculated?

Understanding how your credit score is calculated is the first step to improving it. Here’s a breakdown of the factors that influence your score:

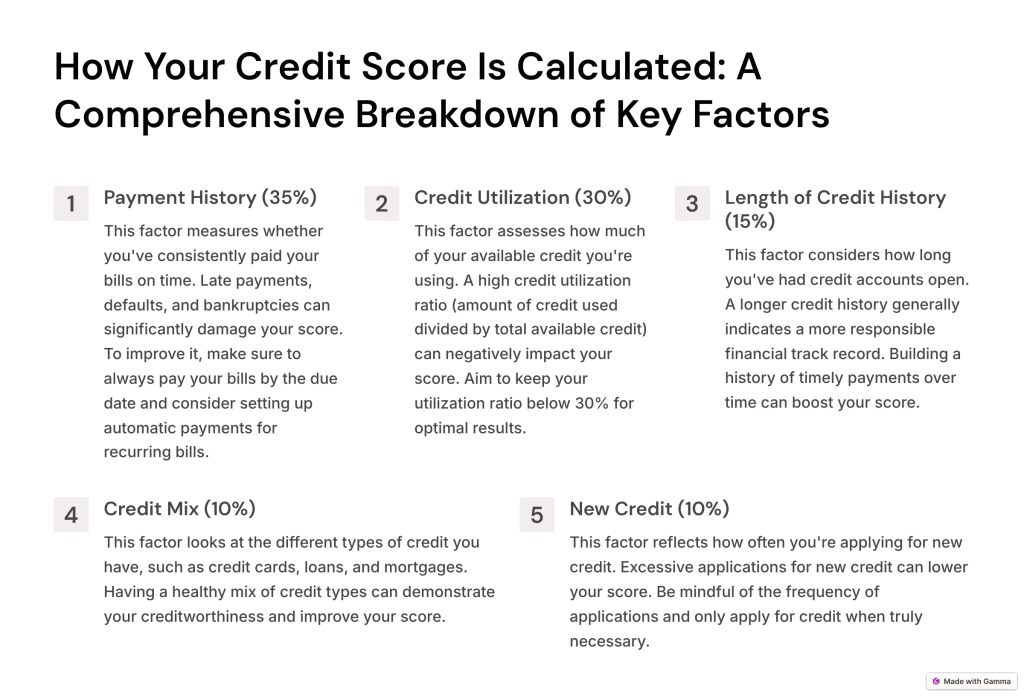

1. Payment History (35%)

- What It Measures : Whether you’ve paid your bills on time. Late payments, defaults, and bankruptcies can significantly hurt your score.

- How to Improve It : Always pay your bills by the due date. Set up automatic payments if necessary.

2. Credit Utilization (30%)

- What It Measures : The percentage of your available credit that you’re using. Experts recommend keeping your utilization below 30%.

- How to Improve It : Pay down balances and avoid maxing out your credit cards.

3. Length of Credit History (15%)

- What It Measures : How long you’ve had credit accounts. A longer history generally boosts your score.

- How to Improve It : Keep old credit accounts open, even if you don’t use them frequently.

4. Credit Mix (10%)

- What It Measures : The variety of credit accounts you have, such as credit cards, loans, and mortgages.

- How to Improve It : Diversify your credit portfolio, but only take on debt you can manage responsibly.

5. New Credit Inquiries (10%)

- What It Measures : How many new credit accounts or inquiries you’ve made recently. Too many inquiries can signal financial distress.

- How to Improve It : Avoid applying for multiple credit accounts in a short period.

Why Does Your Credit Score Matter in 2025?

In 2025, your credit score plays an even bigger role in your financial life. Here’s why it’s so important:

1. Access to Better Loan Terms

A high credit score qualifies you for lower interest rates on loans and credit cards, saving you thousands of dollars over time.

2. Renting and Housing Opportunities

Landlords often check credit scores to assess whether you’ll pay rent on time. A low score could disqualify you from renting your dream apartment.

3. Employment Opportunities

Some employers review credit reports to evaluate your financial responsibility, especially for roles in finance or management.

4. Insurance Premiums

Insurers use credit scores to determine premiums. A good score can help you secure lower rates on auto and home insurance.

5. Future Financial Goals

Whether you’re planning to buy a home, start a business, or invest, a strong credit score opens doors to better opportunities.

How to Check Your Credit Score

Checking your credit score regularly is essential to monitor your progress and spot errors.

Where to Check Your Score

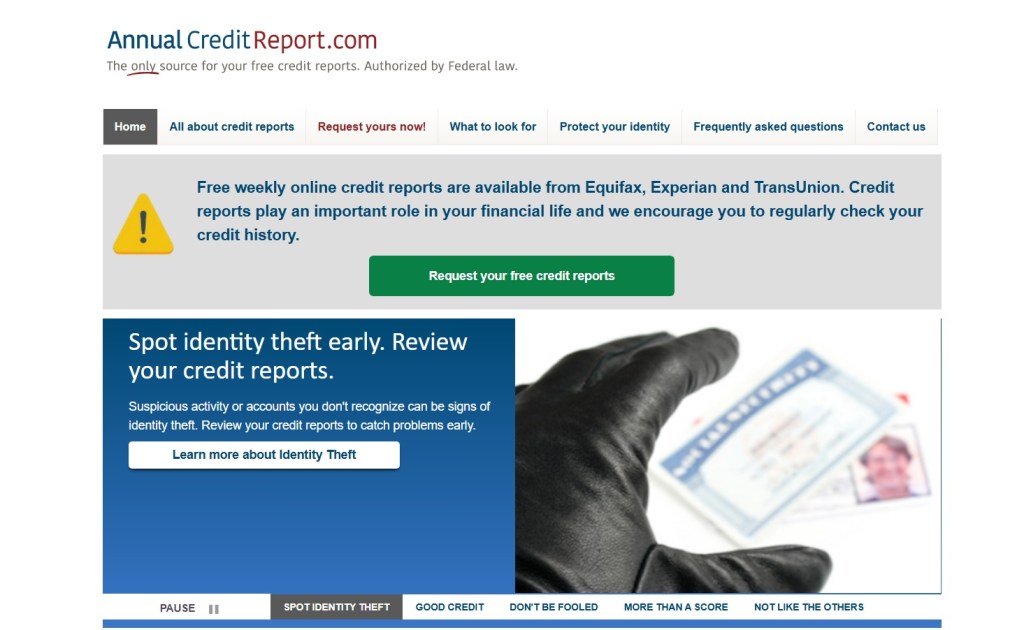

- Free Credit Reports : You’re entitled to one free credit report per year from each of the three major credit bureaus (Equifax, Experian, TransUnion) at AnnualCreditReport.com .

- Credit Monitoring Services : Apps like Credit Karma or Experian offer free credit monitoring and updates.

- Bank or Credit Card Providers : Many banks and credit card companies provide free access to your FICO score.

How Often Should You Check?

- At least once a year to ensure accuracy.

- More frequently if you’re actively working to improve your score.

Common Myths About Credit Scores

There are many misconceptions about credit scores. Let’s debunk some of the most common myths:

Myth #1: Checking Your Credit Score Hurts It

- Reality : Checking your own score is a “soft inquiry” and doesn’t affect your score. Only “hard inquiries” (e.g., when a lender checks your score) have a minor impact.

Myth #2: Closing Old Accounts Improves Your Score

- Reality : Closing old accounts can reduce your credit history length and increase your credit utilization ratio, both of which hurt your score.

Myth #3: Income Affects Your Credit Score

- Reality : Your income isn’t a factor in your credit score. However, having a higher income may make it easier to manage debt responsibly.

Myth #4: Paying Off Debt Immediately Boosts Your Score

- Reality : While paying off debt is beneficial, it takes time for your score to reflect the change.

Actionable Steps to Improve Your Credit Score

Improving your credit score takes time and discipline, but these steps can help you get started:

Step 1: Review Your Credit Report for Errors

- Dispute any inaccuracies, such as late payments that weren’t actually late or accounts that don’t belong to you.

Step 2: Pay Bills on Time

- Set up automatic payments or reminders to avoid missing due dates.

Step 3: Reduce Credit Card Balances

- Aim to keep your credit utilization below 30%. For example, if your credit limit is $10,000, keep your balance below $3,000.

Step 4: Avoid Opening Too Many New Accounts

- Each new account results in a hard inquiry, which can temporarily lower your score.

Step 5: Become an Authorized User

- Ask a family member or friend with good credit to add you as an authorized user on their credit card. Their positive payment history can boost your score.

What to Do If Your Credit Score Is Low

If your credit score is lower than you’d like, don’t panic. Here’s how to recover:

1. Create a Plan

Identify the factors dragging down your score and address them systematically.

2. Negotiate with Creditors

Contact creditors to negotiate settlements or payment plans for overdue accounts.

3. Seek Professional Help

Consider working with a credit counselor or financial advisor to create a recovery plan.

4. Be Patient

Improving your credit score takes time, but consistent effort will yield results.

Celebrate Your Progress and Keep Going

Building and maintaining a strong credit score is a lifelong journey. By understanding how your score works and taking proactive steps to improve it, you’ll unlock better financial opportunities in 2025 and beyond.

Leave a comment