Building a strong financial foundation doesn’t have to take years—it can start in just 30 days. By focusing on key areas like budgeting, debt management, savings, and planning, you can set yourself up for long-term financial success.

In this comprehensive guide, we’ll walk you through how to build a strong financial foundation in just 30 days , with actionable steps you can implement immediately. Whether you’re starting from scratch or looking to refine your financial habits, this plan will help you take control of your money and achieve your goals. Let’s get started!

Week 1: Assess Your Current Financial Situation

The first step to building a strong financial foundation is understanding where you stand today. This week focuses on evaluating your income, expenses, assets, and liabilities to create a clear picture of your financial health.

Day 1–3: Track Your Income and Expenses

Before you can make any meaningful changes, you need to know where your money is going. Tracking your income and expenses is the foundation of financial awareness.

- Why It Matters : Many people overspend simply because they don’t know how much they’re spending or where their money is going. Tracking helps you identify areas where you can cut back.

- How to Do It :

- Use tools like Mint or YNAB (You Need a Budget) to monitor your spending for at least one week. These apps categorize your expenses automatically, making it easier to see patterns.

- If you prefer manual tracking, write down every transaction in a notebook or spreadsheet. Include everything—groceries, coffee runs, subscriptions, and bills.

- Categorize expenses into needs (housing, groceries, utilities) and wants (entertainment, dining out).

Day 4–7: Calculate Your Net Worth

Your net worth is a snapshot of your financial health. It’s calculated by subtracting your liabilities (debts) from your assets (savings, investments, property).

- Why It Matters : Knowing your net worth helps you understand your financial position and track progress over time.

- How to Do It :

- List all your assets: savings accounts, retirement accounts, investments, real estate, and valuable possessions.

- List all your liabilities: credit card balances, student loans, car loans, mortgages, and any other debts.

- Subtract your total liabilities from your total assets.

For example:

- Assets: $50,000 (savings + investments + property)

- Liabilities: $20,000 (credit card debt + student loans)

- Net Worth: $30,000

Week 2: Create a Solid Budget and Emergency Fund

Once you understand your financial situation, it’s time to create a plan to manage your money effectively. This week focuses on building a realistic budget and starting an emergency fund.

Day 8–10: Build a Realistic Budget

A budget is your roadmap for managing money. It ensures you allocate funds for essential expenses, savings, and discretionary spending.

- Why It Matters : A budget prevents overspending and helps you prioritize your financial goals.

- How to Do It :

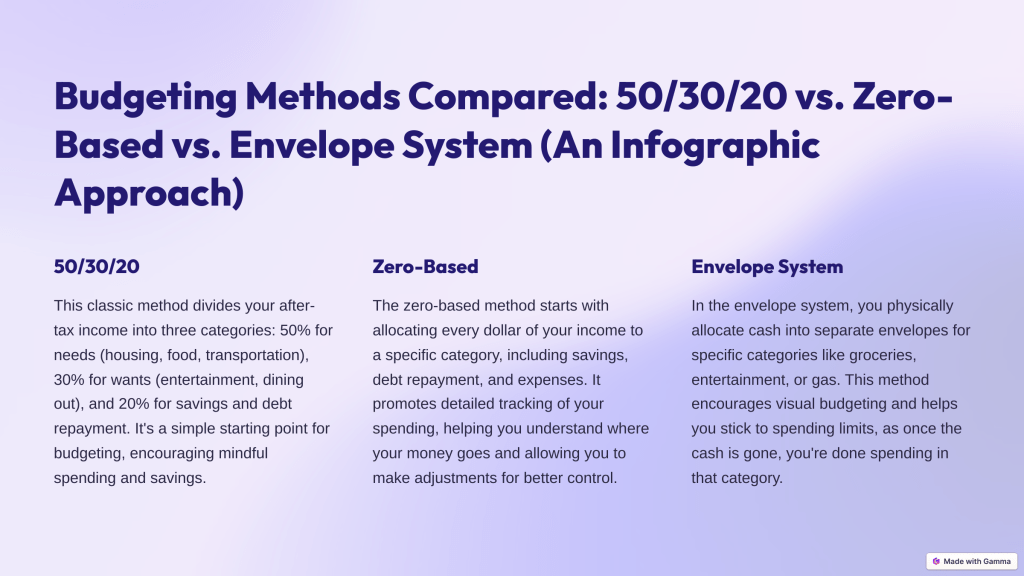

- Follow the 50/30/20 rule : Allocate 50% of your income to needs (housing, groceries), 30% to wants (entertainment, hobbies), and 20% to savings or debt repayment.

- Adjust categories based on your income and goals. For example, if you have high-interest debt, consider allocating more than 20% to debt repayment.

- Use budgeting apps like YNAB or PocketGuard to automate tracking and stay on top of your spending.

Day 11–14: Start an Emergency Fund

An emergency fund is your financial safety net. It protects you from unexpected expenses like medical bills, car repairs, or job loss.

- Why It Matters : Without an emergency fund, you may be forced to rely on credit cards or loans, which can lead to debt.

- How to Do It :

- Aim to save at least $500–$1,000 as a starter emergency fund.

- Automate transfers to a high-yield savings account to make saving effortless.

- Cut unnecessary expenses temporarily to boost your emergency fund contributions.

Week 3: Tackle Debt and Build Credit

Debt can hold you back from achieving financial stability. This week, focus on eliminating debt and improving your credit score.

Day 15–17: Prioritize Paying Off High-Interest Debt

High-interest debt, such as credit card balances, can grow quickly and become overwhelming.

- Why It Matters : Paying off high-interest debt frees up money for savings and investments.

- How to Do It :

- Use the debt avalanche method : Pay off debts with the highest interest rates first while making minimum payments on others.

- Alternatively, use the debt snowball method : Pay off the smallest debts first to build momentum.

- Consider consolidating or refinancing loans to lower interest rates.

Day 18–21: Improve Your Credit Score

Your credit score affects your ability to borrow money, rent an apartment, or even get a job.

- Why It Matters : A good credit score saves you money on interest rates and opens doors to better financial opportunities.

- How to Do It :

- Check your credit report for errors and dispute any inaccuracies.

- Pay bills on time and reduce credit card balances to improve your score.

- Avoid opening too many new accounts at once, as this can lower your score temporarily.

Week 4: Plan for the Future and Automate Finances

The final week focuses on securing your financial future and simplifying money management.

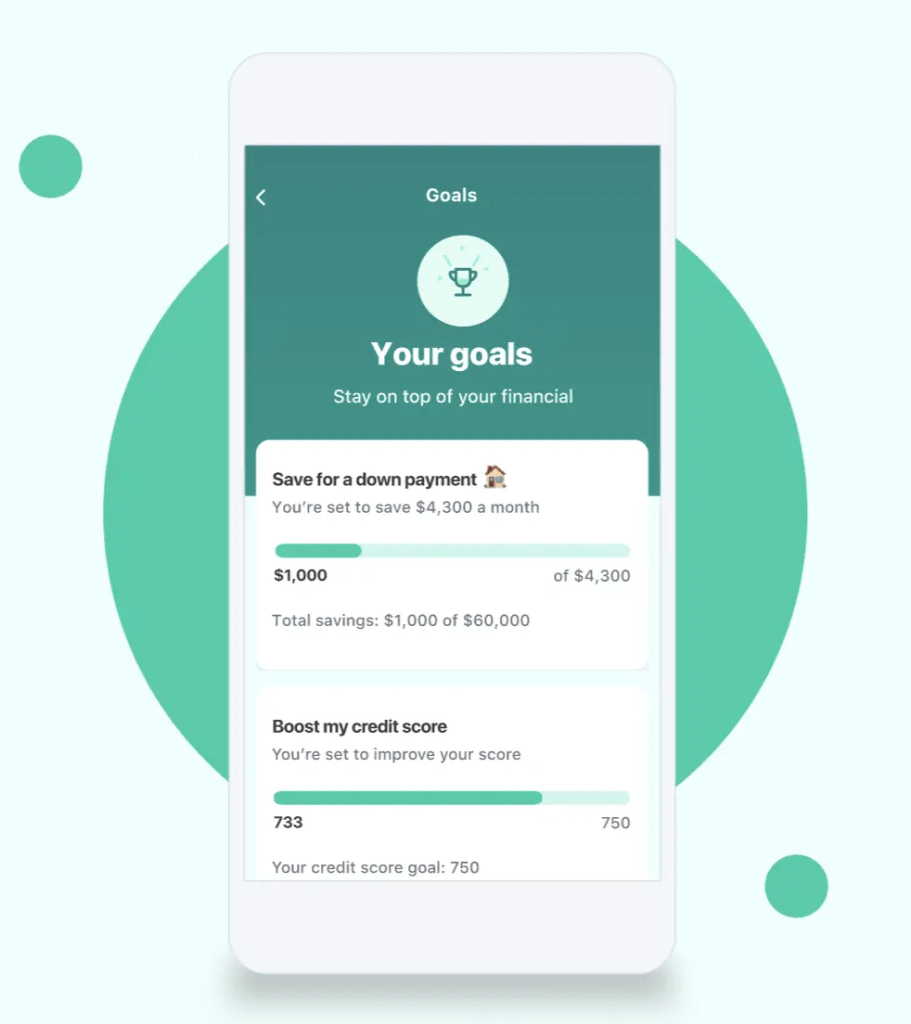

Day 22–24: Set Financial Goals

Setting clear goals gives you direction and motivation.

- Why It Matters : Goals help you stay focused and measure progress.

- How to Do It :

- Write down short-term goals (e.g., save $1,000 for emergencies) and long-term goals (e.g., retire by age 60).

- Break goals into smaller, measurable milestones. For example, if your goal is to save $6,000 in a year, aim to save $500 per month.

Day 25–30: Automate Savings and Investments

Automation ensures consistency and reduces the risk of forgetting important financial tasks.

- Why It Matters : Automating savings and investments removes the need for constant manual effort and helps you stay disciplined.

- How to Do It :

- Set up automatic transfers to savings and investment accounts.

- Use apps like Acorns or Robinhood to start investing small amounts regularly.

- Automate bill payments to avoid late fees and penalties.

Celebrate Your Progress and Keep Going

By following these steps, you’ve laid the groundwork for a strong financial foundation in just 30 days. Remember, financial success is a journey—keep building on these habits to achieve your long-term goals.

Leave a comment